What Is Debt-to-Income Ratio and Why Does It Matter When Buying a Home?

Your debt-to-income ratio, often called DTI, is one of the key numbers lenders review when deciding how much mortgage you may qualify for.

If you are thinking about buying a home in Odenton, Crofton, Gambrills, Bowie, or anywhere in the surrounding Maryland area, understanding your debt-to-income ratio is an important first step. This number helps lenders evaluate how much of your monthly income is already committed to debt payments.

In simple terms, DTI helps answer one major question: can you reasonably handle a mortgage payment on top of your existing financial obligations?

What Is Debt-to-Income Ratio?

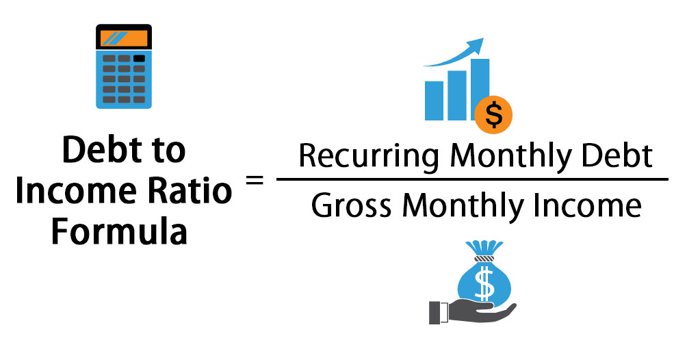

Debt-to-income ratio compares your total monthly debt payments to your gross monthly income. It is expressed as a percentage and gives lenders a snapshot of how much of your income is already being used to pay debt.

Monthly debt payments may include your mortgage or rent, car loans, credit card minimum payments, student loans, personal loans, and other recurring debt obligations.

Income may include salary, bonuses, commissions, self-employment income, retirement income, or other qualifying income sources that a lender can document.

How Is DTI Calculated?

The formula is straightforward:

Monthly Debt Payments ÷ Gross Monthly Income = Debt-to-Income Ratio

For example, if you have $2,000 in monthly debt payments and $5,000 in gross monthly income, your DTI would be 40%.

Example DTI Calculation

| Monthly Debt | Payment |

|---|---|

| Mortgage or Rent | $1,200 |

| Car Loan | $300 |

| Credit Card Payment | $150 |

| Student Loan Payment | $200 |

| Total Monthly Debt | $1,850 |

If your gross monthly income is $5,000, your DTI would be 37%.

Why Does DTI Matter to Mortgage Lenders?

Lenders use DTI to evaluate risk. A lower DTI generally suggests that you have more room in your budget to handle a mortgage payment. A higher DTI may make loan approval more difficult or may limit the loan amount you qualify for.

While every loan program is different, many lenders use 43% as an important guideline. Some loan programs may allow higher ratios depending on credit score, down payment, reserves, loan type, and other compensating factors.

Why DTI Matters for Buyers

Your DTI does more than affect loan approval. It also helps you understand what monthly payment may be realistic. Just because a lender says you can qualify for a certain amount does not always mean that payment will feel comfortable in your actual budget.

Before starting your home search, it is smart to review your debts, income, estimated taxes, insurance, HOA fees, utilities, and maintenance costs. For a deeper look at the real cost of ownership, visit our True Monthly Home Cost Calculator.

Ways to Improve Your DTI

- Pay down credit card balances.

- Avoid opening new debt before applying for a mortgage.

- Increase documented income when possible.

- Consider paying off smaller monthly obligations.

- Review your budget before choosing a target home price.

The Bottom Line

Your debt-to-income ratio is one of the most important numbers in the mortgage process. It affects how much you may be able to borrow, what loan options may be available, and whether your future payment will be manageable.

If you are planning to buy a home in Odenton, Crofton, Gambrills, Bowie, or the surrounding Maryland area, understanding your DTI early can help you make smarter decisions before you start touring homes.

Thinking About Buying a Home?

The Scott Smolen Team can help you understand the local market, evaluate your buying power, and connect you with trusted mortgage professionals.

Contact The Scott Smolen Team